Succession planning: Common pitfalls to avoid

by Samantha Ashenhurst | August 3, 2021 11:45 am

By Danielle Walsh

[1]

[1]

Business owners have a lot on their plate: they are constantly pulled in a million directions and are often busy putting out the proverbial fires that come with the territory. Unfortunately, this is one of the reasons most ignore or put aside succession planning. After all, it’s human nature to postpone complicated tasks—particularly those that may result in pain and conflict. However, while succession planning tends to be viewed as an emotional and painful process (especially in a family business), it doesn’t always have to be that way.

As a business owner who took over operations from her dad, this author is very happy to be in a position where she can continue his legacy and build on his hard work. Recent trends, however, point to situations where operators put their blood, sweat, and tears into their business, but simply do not allocate the same effort to its transition or succession. This could, potentially, lead to flushing a lifetime of hard work down the drain—and business owners have put too much time and work into their operation to see them crumble at the last minute. Further, a rocky (or unsuccessful) transition of ownership can inflict incredible damage on a family unit.

There are a few common pitfalls business owners should be aware of in hopes of helping their business not only survive amidst a transition, but thrive.

Family is family

Right off the bat: if you own a family business, you cannot ignore the family component when developing a succession plan.

Indeed, research shows far too much attention is paid to the technical aspects of a succession plan (e.g. estate freeze, business valuation, tax minimization, trusts, wills, etc.) with little consideration of its non-technical components, including family communication, family values, family dynamics, and family expectations.

This focus on technical components of the process can be easily explained, as family business owners tend to turn to their accountants and lawyers when developing a succession plan. No disrespect intended—I am a chartered professional accountant (CPA) myself—but these professionals are simply not trained on how to deal with the family component of these processes, nor the issues stemming from the family being an integral part of the equation.

Family business practitioners (myself included) would argue the non-technical component (i.e. the family component) is as important—if not more important—than the technical.

Consider this scenario:

I once had a client in his late 80s with three sons in their late 40s and early 50s, all of whom had each been working in the company for most of their adult lives and were more than qualified to run the business. The founder, however, refused to transfer ownership to his sons. He had sought the advice of accountants, lawyers, financial planners, and insurance brokers, but continually received purely technical advice and never obtained the reassurance he needed to make the smooth transition. His fear was the company would crumble under the leadership of his three sons (who did not get along). Ultimately, by implementing competency-based assessments, comprehensive grooming plans, detailed job descriptions, and family business rules/guiding principles, the founder finally felt comfortable transferring his business to his sons. One of the family business rules implemented was a dispute resolution process, which helped improve joint decision-making and avoid conflict. Many of the guiding principles endorsed by this family made it clear the business was an opportunity to be earned and not an entitlement or inheritance. For example, in order to become managers or owners of the business, all family members had to meet stringent criteria. This principle was implemented so dad could make an objective decision based on these established criteria and not on emotions. In this way, we were able to effectively deal with the issue of the three brothers not getting along, while also ensuring the company would continue to be successful.

This example is meant to demonstrate the need to address both the technical and family components when developing a successful succession plan. It is best to deal with the family component (non-technical) first to ensure the technical aspects are in line with and support the family dynamics, the family’s guiding principles, and the family business rules—all of which are part of the overall succession plan, endorsed by the entire family. Having a clear plan for the family component helps reduce the cost and complexities related to the financial, legal, and tax planning.

Beyond a will

[2]

[2]Image courtesy Walsh Family Business Advisory Services

If you have only completed your will and estate planning, there is still plenty of work to be done. Indeed, while many business owners believe these documents will serve as a comprehensive succession plan, what they really are is a plan for death—which is only one of the many exit strategies that needs to be outlined in a succession plan. What about retirement, incapacity, termination of employment, or voluntary exit?

Further, it is rarely recommended to wait until death to transition a business. This type of planning often suggests there are underlying issues the business owner does not want to deal with. While letting go is often cited as one of the most difficult tasks for owners, waiting until death to do so will likely hinder the business (as well as the successors who now must run it). If the goal is to keep the operation going after the owner’s death, the business needs to be transitioned (ideally) far before that happens. There needs to be time to allow the successor(s) to learn and make mistakes while the owner is still there for support, advice, and guidance.

There is also the issue of having a surprise transition in the will. Unfortunately, this happens far too often when all siblings are left with an equal portion of a family-owned business, particularly when some work in the business and others do not. If this arrangement (including who makes decisions and settles disagreements, how to opt out of ownership, how much dividends will be paid, etc.) hasn’t been properly communicated—and, more importantly, properly documented—it is likely to end with family conflict and a struggling business. (It should be noted: when I am faced with these kinds of situations, these key issues are seldom documented properly, leaving siblings who are trying to navigate grief, a business, and dynamics they have never had to deal with.)

To be clear: whether you work as part of a family business or not, there are a lot of items all owners need to agree to (such as exit strategies, dividend policies, hiring and compensation practices, and governance structures) in order to maintain a successful business and working relationship. The ‘succession checklist’ outlined in Figure 1 demonstrates the many items that must come together when developing a comprehensive succession plan. (Again, keep in mind: even if you are not a family business, having guiding principles and rules all owners agree to can certainly help reduce conflict and align expectations.)

Cohesive planning

Another common challenge encountered in succession planning stems from having a detailed plan, but where the individual items are not in sync.

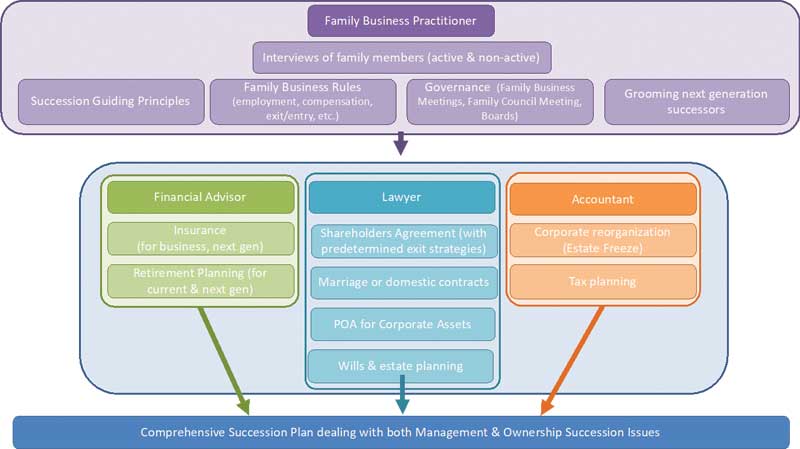

[3]

[3]For example, if two co-owners of a business had their wills written 20 years ago, but recently put a shareholders’ agreement in place with clear exit strategies outlined, chances are their wills and shareholders agreement are not in sync. This, inevitably, will lead to conflict.

While having multiple valid legal documents (e.g. shareholders agreements, wills, trust agreements, etc.) with differing instructions with respect to the shares of the company is not uncommon, it is problematic. This means what the business owner anticipates is going to happen may not be the case.

As seen in Figure 2, all advisors must work together to put a comprehensive and cohesive plan in place; indeed, the lawyer, accountant, financial advisor, and family business practitioner need to ensure all items are in sync. As a family business practitioner, I often quarterback the entire process and then, at the end, review all documentation to ensure it works together.

It is unfortunate how often business owners put all these items in place, but the individual documents are not in line with one another (meaning, the hard work quickly becomes a waste of time and resources). Having one individual in charge of ensuring all documents support the overall succession plan can play an important role in ensuring a successful transition.

Lack of communication

Communication is key when it comes to succession planning. In a family business, this is often a major stumbling block. If a comprehensive family business succession plan is in place, but the entire family is not involved and informed, this is akin to not having a plan at all. Without clear communication of the plan, each family member will have their own expectations; when reality differs, conflict will arise.

The same can be said for a non-family business. Two partners who own equal shares of an operation need to clearly communicate to one another what will happen to their respective ownership should they die, become incapacitated, or want to retire. No one likes to talk about death, but it is surprising how many business partners do not realize they will inherit their partner’s spouse as a co-owner in the case of incapacity or death (as tends to be the case if a clear succession plan outlining the terms and conditions for all exits is not in place).

Further, business owners need to work on this together—it simply cannot be each owner for him or herself. Shared business owners (family or otherwise) must have a clear understanding of what can and cannot be done with their ownership, and this needs to be reflected in wills, shareholders’ agreement, business rules, etc. We often consider someone’s will to be very private, which is why business partners rarely discuss these documents. Co-owners need to communicate this information to each other, as well as to their successors and to their respective families. When the succession plan is not communicated clearly, it is often seen as not existing at all.

If the time and resources are spent putting a comprehensive succession plan in place, the same consideration should go into communicating it to those impacted. Business owners should take pride in sharing their succession plans with partners, potential successors, family members, and anyone else involved.

Taking action

My dad has always said business owners have a moral obligation to put a plan in place to safeguard their family, other owners, and the business itself. This is a major undertaking and often feels overwhelming. That said, it is not meant to be an item to simply check off your list; rather, succession planning is a process which is impacted by all major life events (marriage, new family, retirement, death, etc.). The sooner you get going, the easier it will be!

If you are part of a family business, be aware you need to consider the family component first, otherwise the plan is unlikely to meet all your objectives (business continuity and family harmony). Having updated wills and an estate plan is also important, but keep in mind wills are a small part of the plan. These documents need to support your overall succession strategy and be in line with your shareholders agreement, exit strategies, business rules, and so forth. Finally, if you have done the hard work of putting these items in place, you owe it to yourself, your business, and your family to share this plan.

In closing, consider this other thought, courtesy of my dad: once you have successfully completed your comprehensive succession plan, celebrate your achievement by planning a family party!

[4]Danielle Walsh is founder of Walsh Family Business Advisory Services, a consulting company specializing in helping family-owned and operated businesses navigate management and ownership succession. She is a certified public accountant (CPA), chartered accountant (CA), and holds certificates in family business advising and family wealth advising from the Family Firm Institute (FFI). Walsh developed her philosophy and desire to help family businesses from her father, Grant Walsh, who has worked as a family business practitioner for the last 25 years. She and her father recently published a book titled A Practical Guide to Family Business Succession Planning: The Advice You Won’t Get from Accountants and Lawyers. Walsh also currently teaches the first family business course offered at the undergraduate level at Carleton University in Ottawa. She can be reached at danielle@walshfbas.com[5].

[4]Danielle Walsh is founder of Walsh Family Business Advisory Services, a consulting company specializing in helping family-owned and operated businesses navigate management and ownership succession. She is a certified public accountant (CPA), chartered accountant (CA), and holds certificates in family business advising and family wealth advising from the Family Firm Institute (FFI). Walsh developed her philosophy and desire to help family businesses from her father, Grant Walsh, who has worked as a family business practitioner for the last 25 years. She and her father recently published a book titled A Practical Guide to Family Business Succession Planning: The Advice You Won’t Get from Accountants and Lawyers. Walsh also currently teaches the first family business course offered at the undergraduate level at Carleton University in Ottawa. She can be reached at danielle@walshfbas.com[5].

- [Image]: https://www.jewellerybusiness.com/wp-content/uploads/2021/08/opener.jpg

- [Image]: https://www.jewellerybusiness.com/wp-content/uploads/2021/08/1_Succession-Checklist.jpg

- [Image]: https://www.jewellerybusiness.com/wp-content/uploads/2021/08/2_Comprehensive-Succession-Plan.jpg

- [Image]: https://www.jewellerybusiness.com/wp-content/uploads/2019/12/Walsh_Headshot_crop.jpg

- danielle@walshfbas.com: mailto:danielle@walshfbas.com

Source URL: https://www.jewellerybusiness.com/features/succession-planning-common-pitfalls-to-avoid/